Retirement means different things to different people. For some, it’s freedom from work and time to enjoy life. For others, it’s a phase filled with worry about money and security. But one thing is common, everyone wants a stable and comfortable retirement.

For years, 1 crore has been seen as the magic number for retirement. Many believe reaching that figure means lifelong financial security. But is that true in today’s world? With inflation, longer life spans, and changing lifestyles, the idea of 1 crore being “enough” has become more complicated.

In this blog, we’ll break down whether 1 crore can actually sustain a good retirement today, how inflation has changed the picture, and what you can do to prepare better for your golden years.

Retirement is seen as a time for relaxation, travel, and hobbies. For years, 1 crore has been the magic number, symbolizing comfort and security. In the past, it was enough to live off returns and feel financially independent.

But today, with inflation and rising costs, the question is, is 1 crore still enough? For many young earners, it feels like the final goal, but it’s really just a milestone. Retirement planning needs regular updates to match future needs.

What looks big at 25 may not be enough at 55. Healthcare, lifestyle changes, and inflation all mean a larger corpus is required. The idea of 1 crore gives psychological comfort, but without real planning, it may not secure your retirement.

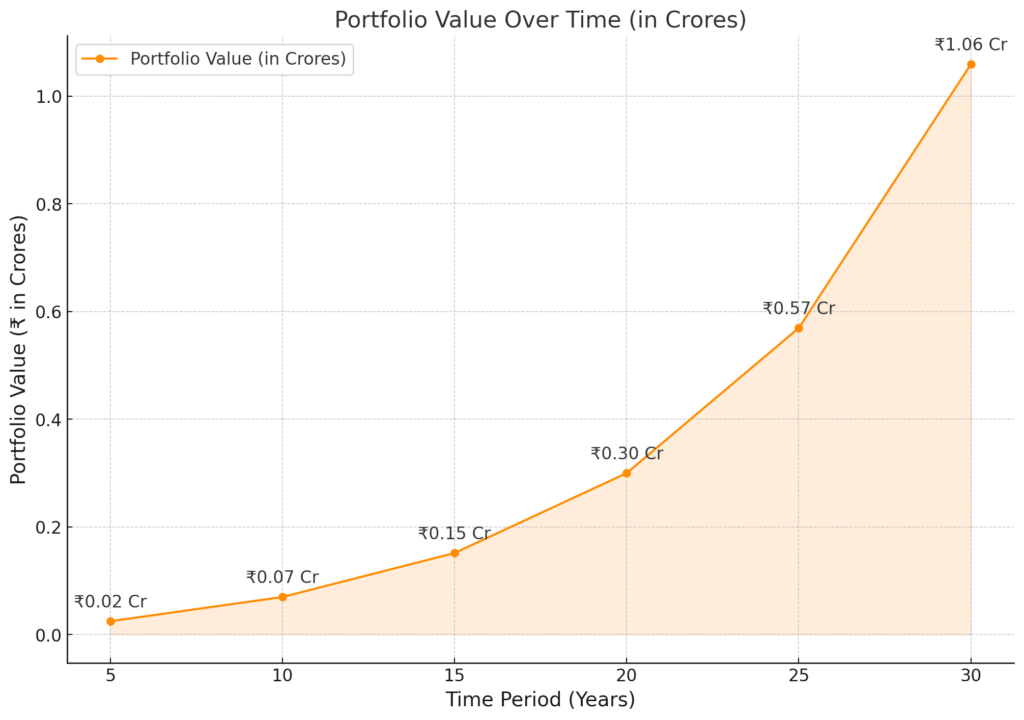

Reaching 1 Cr. Retirement Corpus with SIPs

Systematic Investment Plans (SIPs) are one of the most effective ways to build a retirement corpus. By investing a fixed amount regularly in mutual funds, you benefit from rupee cost averaging and the power of compounding. Even small contributions can grow big if you start early and stay consistent. The key is to stay invested and avoid pulling money out too soon, as that can break the compounding cycle and reduce your gains.

The SIP of 3,000 rupees per month over 30 years, assuming a 12% return, would result in a corpus of around 1.05 crore. But considering the future value of this amount, is it enough?

Reaching 1 Cr. Retirement Corpus with SIPs

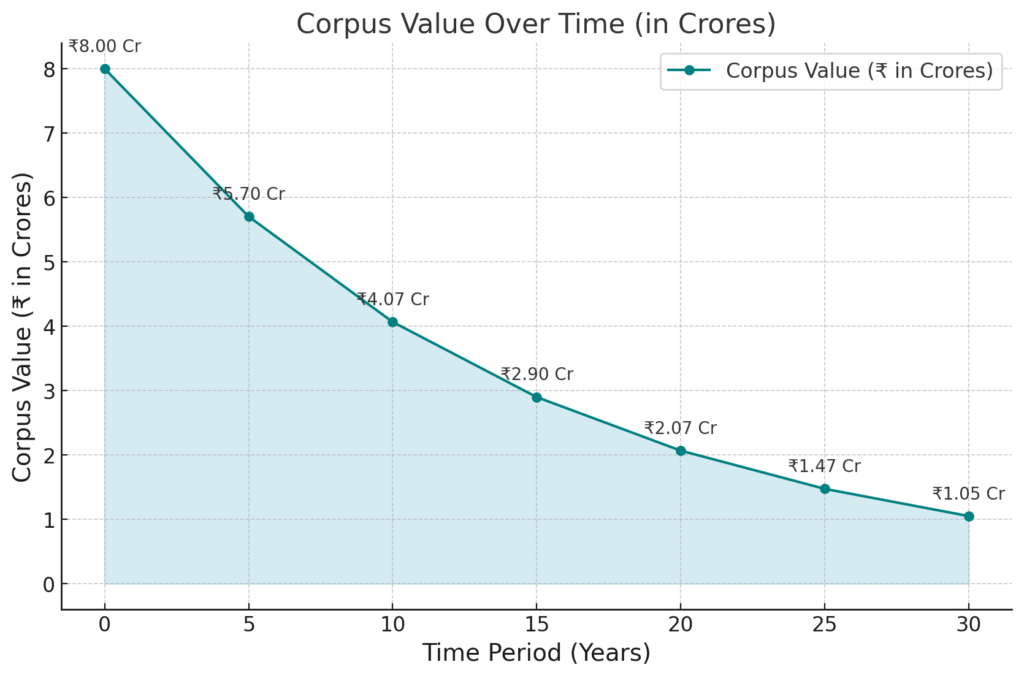

While aiming for 1 crore as a retirement goal may sound tempting, it’s important to understand its future value. Inflation reduces the purchasing power of money, so 1 crore today won’t be worth the same later. For example, at 7% inflation, 1 crore in 30 years will be worth only about ₹13.1 lakhs in today’s value, nearly 7.6 times lower than what you planned for.

Value of Desired Corpus after Inflation

This gap shows why inflation must be part of retirement planning. Ignoring it can leave you with a big shortfall and much less financial security than you expected.

What is the equivalent Corpus & SIP?

Building Retirement Corpus with SIP

To keep the same purchasing power, you may actually need around ₹8 crore for retirement. That means investing about ₹22,830 per month for 30 years at 12% returns. It may sound tough, but this shows why starting early and adjusting your goals is key. If you don’t factor in inflation, your savings may fall short. A good habit is to increase your SIP every year, even by 10%, your money keeps up with rising costs.

As your income grows, your SIPs should grow too. This way, you fight inflation and use the power of compounding to build a solid retirement cushion.

Conclusion

Retiring with 1 crore once meant financial success, but today, it may not be enough. Inflation, rising costs, and longer life spans have reduced its true value. That’s why you need a flexible and realistic financial plan for a secure retirement.

Planning isn’t just about chasing a round number. It means calculating your real retirement needs but considering your income, expenses, insurance, lifestyle goals, and investments. Only then can you know the actual corpus required. Simply investing ₹2,000 or ₹3,000 a month won’t work if your income is much higher, say ₹1 lakh per month. To stay on track, you must set bigger goals, save more, and review your plan regularly.

True financial security comes from discipline, consistency, and adaptability. By starting early and adjusting as you grow, you can achieve the financial freedom needed for a stress-free retirement.